I've left Devon. I don't shop at 7-11. Celsius advised to file, for chapter 11.

I know, another crap rhyme.

Good evening everyone.

Sorry, it’s a bit late (again), I’m in the middle of moving country and currently sitting on the floor of my unfurnished flat, writing this newsletter.

Celsius’s similarities to bitcoNEEEECCTT!!

Let’s face it, not only has this newsletter lacked consistency, but it also lacked some sort of continuity.

This is my attempt of bringing continuity to it (which is ironic as this is the last one for the time being).

Last week I wrote about the tragic trajectory craptos have been on due to an imminent recession, fed hikes, and freezing of crapto withdrawals from Binance and the Celsius Network.

I pointed out the possible issues that Celsius Network could face from a potentially insolvent balance sheet to its treacherous capital structure. However, I missed something rather crucial (and hilarious, it gave me 2017 crapto bubble PTSD, hence the meme) which was picked up on “Our World This Week” by Capitalist Exploits. The similarity between BitConnect and Celsius is the interest rates promised from depositing crapto. If you wanna catch up on the iconic BitConnect saga, read here.

Keeping it concise: BitConnect promised double-digit returns on money deposited, and customers could compound it. You can’t compound with Celsius, so a slight deviation there. BitConnect collapsed in 2017; it was a global Ponzi scheme.

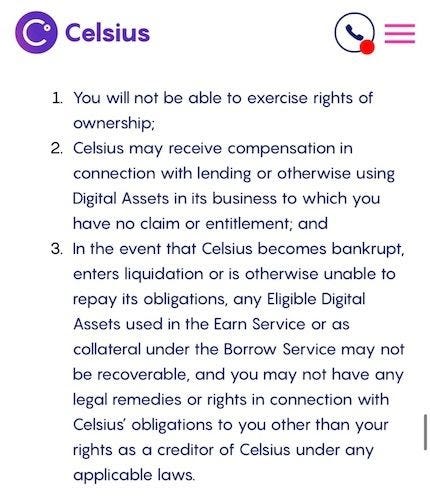

Anyway, now you know what happened with BitConnect, moving back to Capitalist Exploits’ finding - Capitalist Exploits points out Celsius’s fine print:

I mean, reading it I came away thinking that “I own nothing and Celsius has no obligation to me” if I put money in it.

To be honest, I couldn’t find the example above but, in my endeavour to do so, I came across this yummy Cease and Desist Order filed by the New Jersey Bureau of Securities in 2021.

This doc gave me a much better understanding of Celsius. So customers deposit their crapto in return for interest-earnings accounts (a security, Celsius calls them Earn Rewards accounts), this allows Celsius to fund its lending operations whilst its customers earn passive income on their hard-earned craptos.

These interest-earning accounts (which is in effect, a security) unsurprisingly, due to lack of regulation in the sector, aren’t protected by the Securities Investor Protection Corp (SIPC), or insured by the Federal Deposit Insurance Corp (FDIC), nor by the National Credit Union Administration (NCUA). All that this means is that, if your money is in there and you throw a hissy fit because you don’t get the interest rate you hoped for, or they stop you from withdrawing it (lol), or worse it just… vanishes like with Bitconnect - it’s all on you buddy. No one’s going to help you.

Despite this compelling fact found in 2021 when the Cease and Desist order was filed, more than $14 billion was held by Celsius in Earn Rewards accounts which at the time, they failed to register.

Reading the whole document, Celsius sheds very little light on explaining how it’s able to pay such interest, which I think is at the precipice of this (my) curiosity. The only explanation of how the “daily periodic rate” (the interest rate that is paid when a customer deposits crapto into their Earn Rewards account) is calculated for when a customer deposits bitcoin (for example) in their Earn Reward account is this:

“calculated by dividing the then-applicable annual reward rate by three hundred and sixty four days (364); then it is further divided in the hour, minute, and second of that day” - From the Cease and Desist Filing

Like, great. Thanks for explaining how years work and also primary school math. I feel soooooo much better about handing over $100k worth of bitcoin that I made from yolo’ing money from my nan when I was 13. (I’m being facetious, I don’t have $100k RIP).

So yeh, the picture looks odd. And if it is legitimate, I wanna know where the hell Celsius is investing to be able to pay its Earn Reward customers ~17% interest per annum.

The conclusion from the filing is that Celsius was banned from New Jersey.

But “this is old gossip, this was in 2021. Stop stirring the pot!” you say.

Ok. Finneeee. What’s going on now then?…

Just a cheeky Chapter 11 wafting about. My speculation on their insolvency problems last week looks much less speculative, not that it was a tough guess.

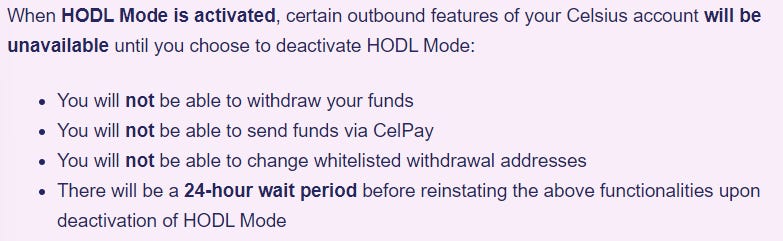

Celsius’s lawyers are pushing for the firm to file for bankruptcy but Celsius is playing one final roll of the dice to remain solvent. They are doing this by countering their lawyer’s advice using the notion that it’s not what its customers would want and they’d show their support by implementing “HODL Mode” on their accounts. *sigh* F*ck. Me.

Basically “HODL Mode” is where customers opt into freezing withdrawals from their own accounts. I mean, Celsius did that the other week, so if someone activates HODL Mode it makes zero practical difference, lol. I guess they didn’t read this on Celsius’s website, note the first bullet point:

As I said, you’re literally just freezing withdrawals from your own account, well done you HODL’er. You’re HODL Mode squared now.

I have no idea how much debt they’d need to restructure, but just to be clear: As much debt as possible will be paid off first if they do file for Chapter 11, and then all the sweet little HODL’ers will get a few crumbs of the pie if they’re lucky. That’s usually how these things pan out. Again, it’s just my speculation, I have no inside knowledge on the situation, just to be clear.

Honestly, I just can’t wait to see how this develops. Especially since it’s reported that Goldman Sachs would broker (some people say buy, I’m really not sure…) Celsius’s assets at a huge discount of $2 billion only if Celsius files for bankruptcy. Will Goldman broker, in effect, a debt/equity Swap? They can’t be buying equity in Celsius; it goes to zero when they file for chapter 11 bankruptcy? I don’t know. I’m not a distressed debt/asset investor. I need to read more Moyer.

Anyways, that’s about it folks. I sadly have to say bye for now, compliance is a hugely important thing in finance and I’m afraid I’ll have to put the Benatar Report on hold due to compliance reasons.

But, before I go, I’d like to introduce you to some of what I read and listen to regularly:

Reading:

Newsletters:

Bloggers

Listening:

Podcasts

Take it easy lads and ladettes.